The heavy vehicle industry in Mexico is going through one of its most challenging periods in recent years. Official data from theNational Institute of Statistics and Geography (INEGI) and the National Association of Bus, Truck, and Tractor Manufacturers (ANPACT) show that heavy truck production fell 49% in February 2026 compared to the same month last year, reflecting a widespread decline that also hit exports and domestic sales.

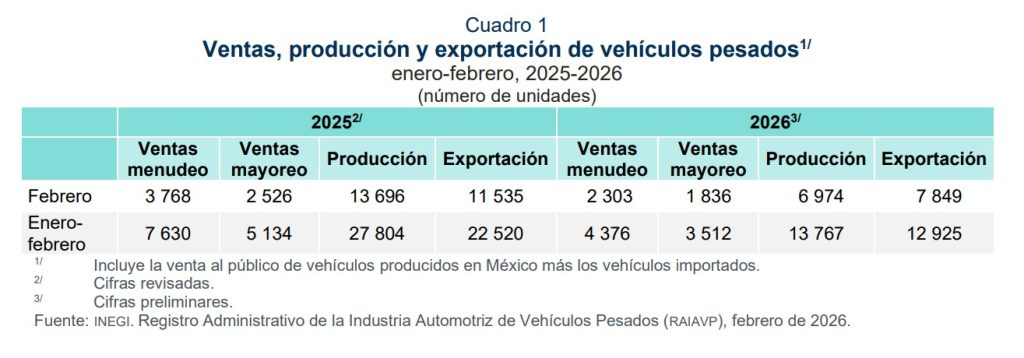

In February, companies operating in Mexico produced 6,974 units, far below the 13,696 units recorded in February 2025, marking the sector’s lowest monthly output in roughly five years.

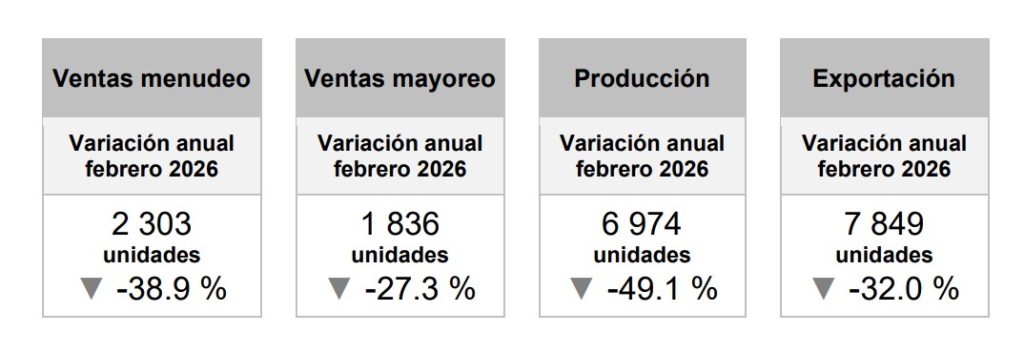

The decline was not limited to production. Exports dropped 32%, while wholesale sales fell 27% and retail sales dropped 39% year-on-year, highlighting a significant slowdown across the heavy transport value chain.

You may also like | SynergEV Presents Its 360° Solution for Unlimited Charging Infrastructure in Mexico and Latin America

Diesel still dominates production

Of the total vehicles produced in February, 6,739 were cargo trucks and 235 were passenger buses, reflecting the typical production structure of Mexico’s heavy vehicle industry.

In terms of powertrain, diesel continues to dominate. Out of 6,974 units produced, 6,972 ran on diesel, with only one electric vehicle and one natural gas vehicle produced.

This illustrates that, despite growing global discussions on transport decarbonization, electrification in Mexico’s heavy truck segment remains minimal, mainly due to high technology transition costs and limited infrastructure for alternative fuels.

Exports also decline sharply

The external market, traditionally the main driver of Mexico’s heavy truck industry, also showed weakness.

In February 2026, Mexico exported 7,849 heavy vehicles, down 32% from 11,535 units exported in February 2025. Although this was a partial rebound from January 2026, when 5,076 units were shipped, the volume remains well below recent records.

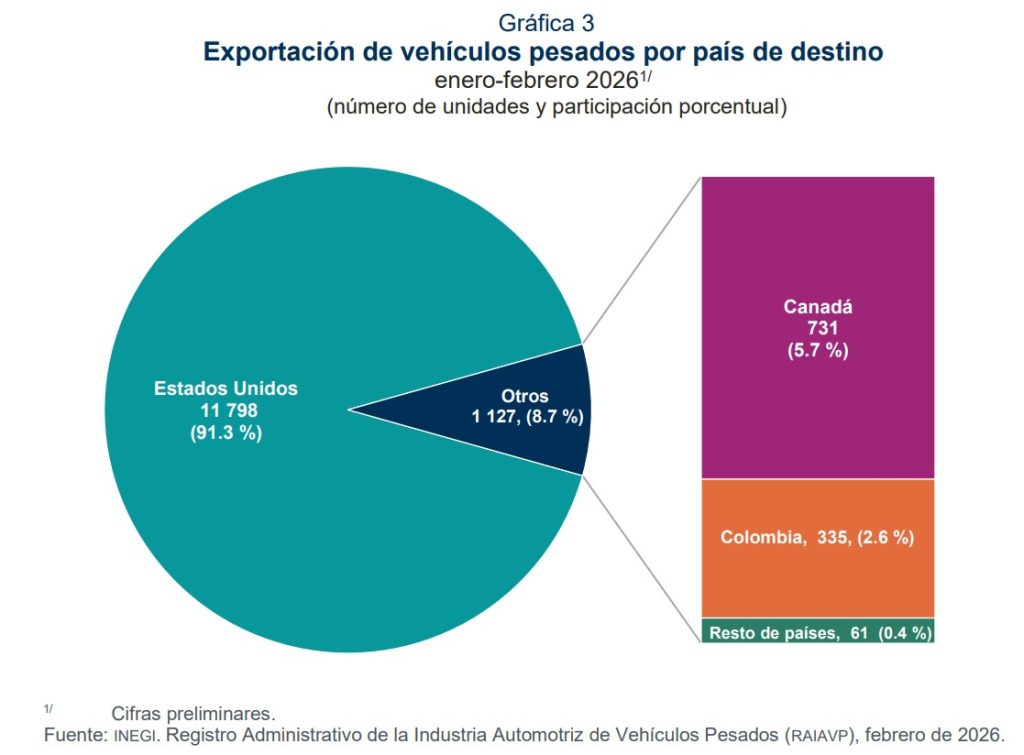

The United States remains the main destination, absorbing 7,015 units, followed by Canada with 498 units. Colombia is gradually emerging as a market for Mexican heavy vehicles.

As with production, diesel accounted for nearly all exports (7,847 units), with only one electric truck and one natural gas vehicle.

Domestic market in Mexico continues to decline

Weakness in the domestic market has also weighed on the sector.

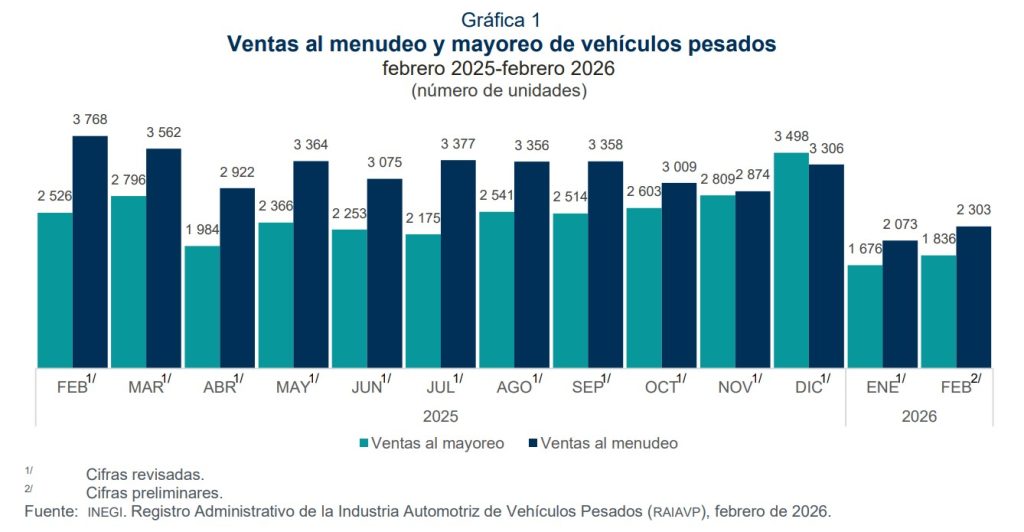

Wholesale sales reached 1,836 units in February, a 27.3% drop year-on-year, while retail sales totaled 2,303 units, down 38.9% compared to February 2025.

In the first two months of 2026, retail sales totaled 4,376 vehicles, a 42.6% decline from the same period last year.

According to the Mexican Association of Automotive Distributors (AMDA), the market has now recorded 14 consecutive months of year-over-year declines, reflecting a challenging environment for fleet renewal.

Used truck imports pressure the market

A growing influx of used trucks from the United States is another major concern, putting pressure on domestic sales.

Industry estimates suggest that for every 100 new trucks sold in Mexico, around 64 used units enter the market, many with high mileage or poor mechanical condition.

Manufacturers warn that this dynamic distorts the market, reduces sales of new vehicles, and could impact road safety and emissions.

Calls for stronger regulation

In response, ANPACT has urged the federal government to review regulatory mechanisms governing the import of used heavy vehicles.

The association called on the Ministry of Finance, Mexican Customs Agency, Ministry of Economy, and Ministry of Environment to strengthen controls to prevent the entry of vehicles that do not meet adequate standards.

The sector also noted that tariffs under Section 232 of U.S. trade law have created uncertainty for the regional automotive industry, compounding the effects of ongoing negotiations under the United States-Mexico-Canada Agreement (USMCA).

First two months show historic decline

Cumulative performance in the first two months of 2026 confirms the magnitude of the slowdown. Between January and February, 13,767 heavy vehicles were produced, down 50.5% from 27,767 units in the same period in 2025.

Exports totaled 12,925 units, a 42.6% year-on-year decline.

Despite the challenges, the industry remains hopeful that greater trade stability and stronger regional coordination will help production recover gradually. Manufacturers emphasize that integration of North American supply chains and stronger regional industrial policies will be crucial to reversing the negative trend and maintaining the sector’s competitiveness.

A Tour to Consolidate Transformation

The success of the summit in San Pedro Garza García is just the beginning of a key year for mobility in the region. Latam Mobility will continue its work of connection and dissemination throughout 2026 with a tour of the main markets in Latin America.

Through its stops in Mexico City, Brazil, Colombia, and Chile, the platform will continue to promote a collaborative approach to accelerate the transition to cleaner, more efficient, and more inclusive transportation systems, positioning Latin America as a relevant player in sustainable mobility at the global level.

Be part of the movement that is accelerating Latin America’s energy and urban transformation. If you would like to learn more about how to participate and positioning options, click here.