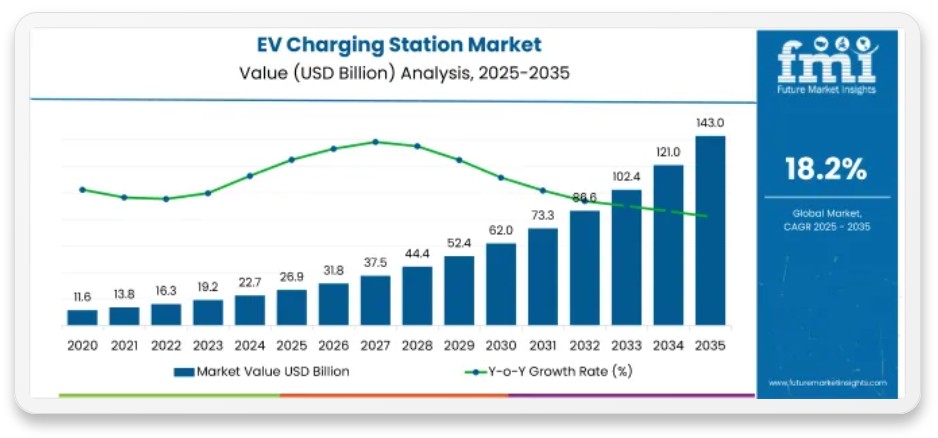

The global electric vehicle (EV) charging station market is poised for explosive growth over the next decade. According to a report from Future Market Insights (FMI), the sector will climb from USD 26.87 billion in 2025 to USD 143 billion in 2035, representing a blistering 18.2% compound annual growth rate (CAGR) over the forecast period.

This surge is fueled by the rapid uptake of electric vehicles, massive government investments in charging infrastructure, and the rollout of faster, smarter charging tech built to handle the large-scale electrification of transportation.

EV charging stations are evolving beyond their traditional role as simple power sources and are transforming into smart mobility hubs. Today’s systems pack real-time monitoring, intelligent charge management, renewable energy integration, and vehicle-to-grid (V2G) capabilities. As EV ownership takes off globally, reliable charging access is rapidly becoming a linchpin for sustainable mobility.

You might also be interested in | CATL Unveils TENER Sodium: The First GWh-Scale Commercial Storage Solution With Sodium-Ion Batteries

Drivers and Strategic Market Shifts

The surging uptake of EVs is creating massive demand for charging infrastructure across residential, commercial, fleet, and public transit settings. Governments around the world are ramping up funding to improve charger accessibility along highways, urban corridors, and rural transport networks.

At the same time, advances in ultra-fast charging tech, IoT-enabled platforms, and intelligent energy management systems are slashing downtime and refining the user experience.

Key growth drivers include the rising adoption of passenger and commercial EVs, government infrastructure programs, the expansion of DC ultra-fast networks, the integration of IoT-enabled charge management, growing demand for residential and workplace solutions, renewable-energy-powered stations, and the spread of V2G and smart grid integration.

Nikhil Kaitwade, Analyst at Future Market Insights, notes that the market is entering a phase of massive infrastructure expansion as governments, utilities, and private operators accelerate their push for charging accessibility.

Kaitwade adds that operators who deliver rock-solid fast-charging hardware, smart energy management software, and top-tier station uptime will be the big winners over the next decade.

That said, the market isn’t without its headaches. Challenges include grid capacity constraints, sky-high deployment costs, charger interoperability issues, land acquisition hurdles, and the sheer complexity of keeping vast charging networks up and running.

Segments and Regional Outlook

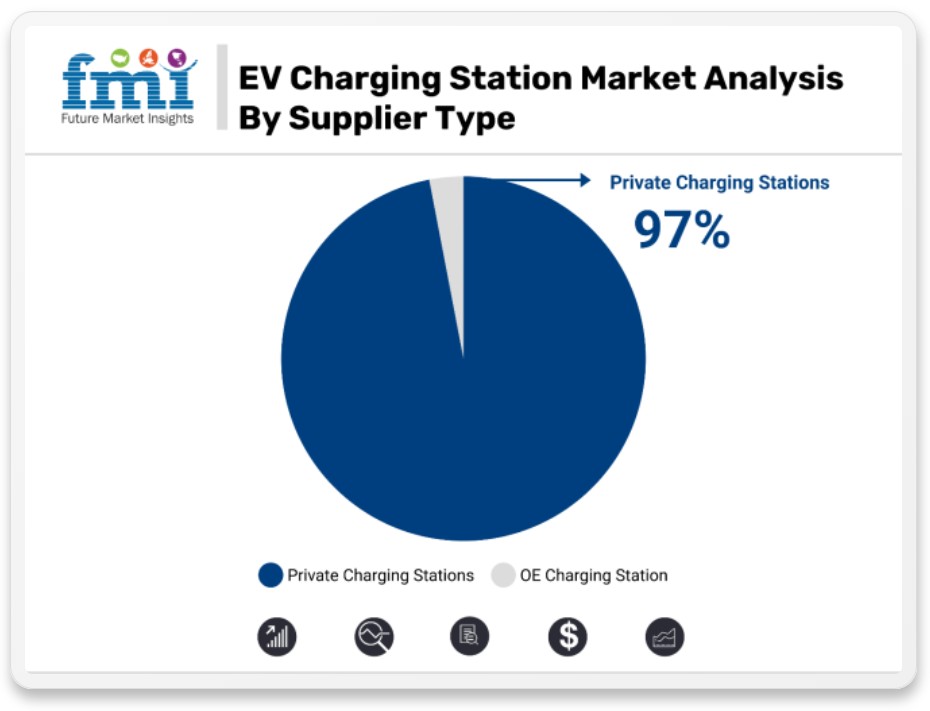

The private station segment will take the lion’s share by provider type, accounting for over 97% of market share in 2025, thanks to the growing installation of chargers in homes, workplaces, and fleets across major EV markets.

Meanwhile, residential charging stations are the clear frontrunner in the ownership model segment with over 94% share, driven by consumer preference for overnight charging, cheaper off-peak electricity rates, and better incentives for home charger setups.

On the tech side, AC stations will remain the go-to for residential and parking applications, while DC fast-charging infrastructure continues its rapid expansion along highways and commercial transport routes.

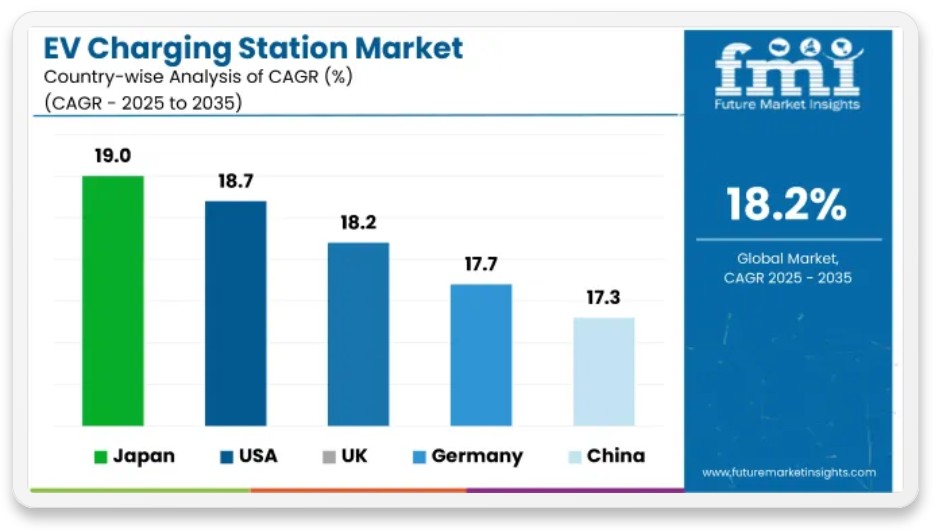

Regionally, Japan is leading the pack at the country level, backed by heavy investments in ultra-fast highway charging. The United States is seeing a strong surge thanks to federal charging programs and private sector cash. China keeps dominating global charger deployment with an extensive fast-charging network buildout. Germany is benefiting from robust EV adoption and government subsidies, while the United Kingdom is pouring money into smart charging and residential infrastructure.

Countries like Japan, the U.S., China, Germany, and the UK are emerging as the prime battlegrounds for next-generation charging infrastructure and intelligent energy management solutions.

Global Players and Differentiation Strategies

The EV charging station market is moderately fragmented, featuring a mix of global charging providers, power electronics manufacturers, energy heavyweights, and mobility tech firms.

Key players include Tesla, ABB, BYD, Schneider Electric SE, Siemens AG, Robert Bosch GmbH, Delta Electronics, Tritium, Wallbox, Eaton, Webasto, General Electric, Star Charge, and Efacec.

Competitive strategies are increasingly focused on:

- Expanding ultra-fast charging networks;

- Developing smart charging software and load-balancing platforms;

- Integrating renewable energy sources and energy storage systems;

- Rolling out IoT-enabled monitoring and predictive maintenance;

- Forging strategic partnerships with automakers, utilities, and fleet operators;

- Investing in wireless and autonomous charging technologies.

In short, the EV charging station market isn’t just seeing massive growth in raw numbers—it’s undergoing a deep qualitative shift that makes it a strategic pillar of the entire mobility ecosystem. The USD 143 billion projection says it all: transportation electrification is no longer an aspiration; it’s a global sprint, and charging infrastructure is every bit as critical as vehicle manufacturing itself.

The road to 2035 is mapped out, and companies that put their chips on robust, scalable, and sustainable solutions today are quite literally building the energy arteries for tomorrow’s travelers.

A Year 2026 of Consolidation for Mobility

The Latam Mobility 2026 Tour will arrive in Santiago, Chile, on August 25, bringing together experts and strategic players to further strengthen the sustainable mobility ecosystem in the region.

The tour will end in Mexico City on October 12 and 13, alongside the Climate Economy Forum, in a meeting that will bring together sector leaders to continue driving the transition toward more efficient, sustainable, low‑emission transportation systems in Latin America.

The transition is already underway. The Latam Mobility 2026 Tour will be the meeting point to accelerate decisions, connect key players, and collaboratively build sustainable mobility in Latin America.